4900 Via Los Santos | Santa Barbara, CA 93111

5 BEDROOMS | 6 BATHS

OFFERED AT $3,395,000

Viewing entries tagged

santa barbara ca homes for sale

4900 Via Los Santos | Santa Barbara, CA 93111

5 BEDROOMS | 6 BATHS

OFFERED AT $3,395,000

Excited for our clients who scored this amazing fixer home in a desirable Goleta neighborhood.

Sold for $1,205,000

125 Gray Avenue | Santa Barbara, CA 93101

2 BEDROOMS | 2 BATHS

OFFERED AT $1,799,000

Listing agent: David Kim

Listing Brokerage: Village Properties

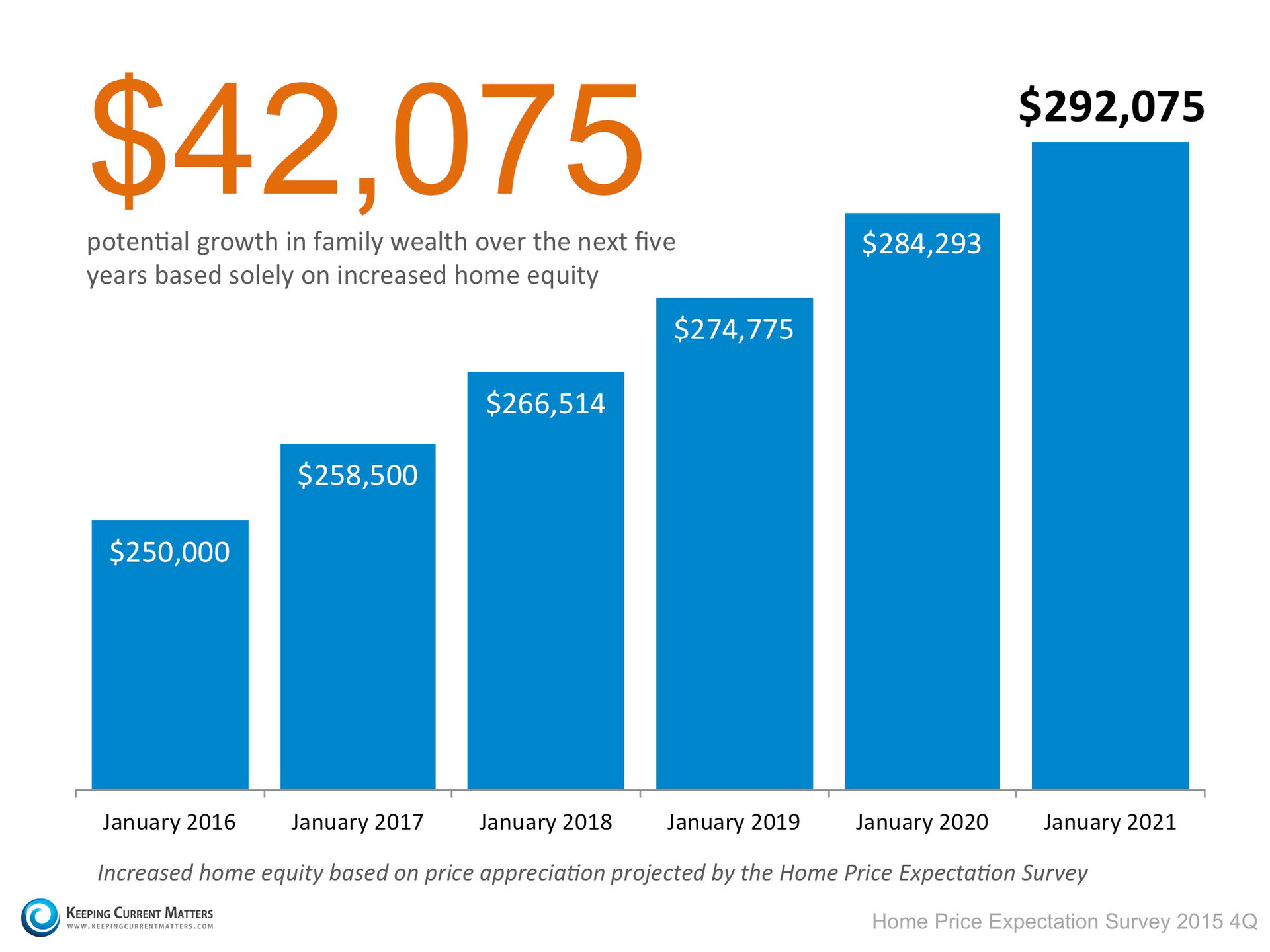

As the economy continues to improve, more and more Americans are seeing their personal financial situations also improving. Instead of just getting by, many are now beginning to save and find other ways to build their net worth. One way to dramatically increase their family wealth is through the acquisition of real estate.

As the economy continues to improve, more and more Americans are seeing their personal financial situations also improving. Instead of just getting by, many are now beginning to save and find other ways to build their net worth. One way to dramatically increase their family wealth is through the acquisition of real estate.

For example, let’s assume a young couple purchases and closes on a $250,000 home in January. What will that home be worth five years down the road?

Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts and investment & market strategists every quarter. They ask them to project how residential prices will appreciate over the next five years. According to their latest survey, here is how much value that $250,000 house will gain in the coming years.

Over a five year period, that homeowner can build their home equity to over $40,000. And, in many cases, home equity is large portion of a family’s overall net worth.

If you are looking to better your family’s long-term financial situation, buying your dream home might be a great option.

![Home Equity Increasing as Home Prices Rise [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/12/Equity-Infographic-KCM1.jpg)

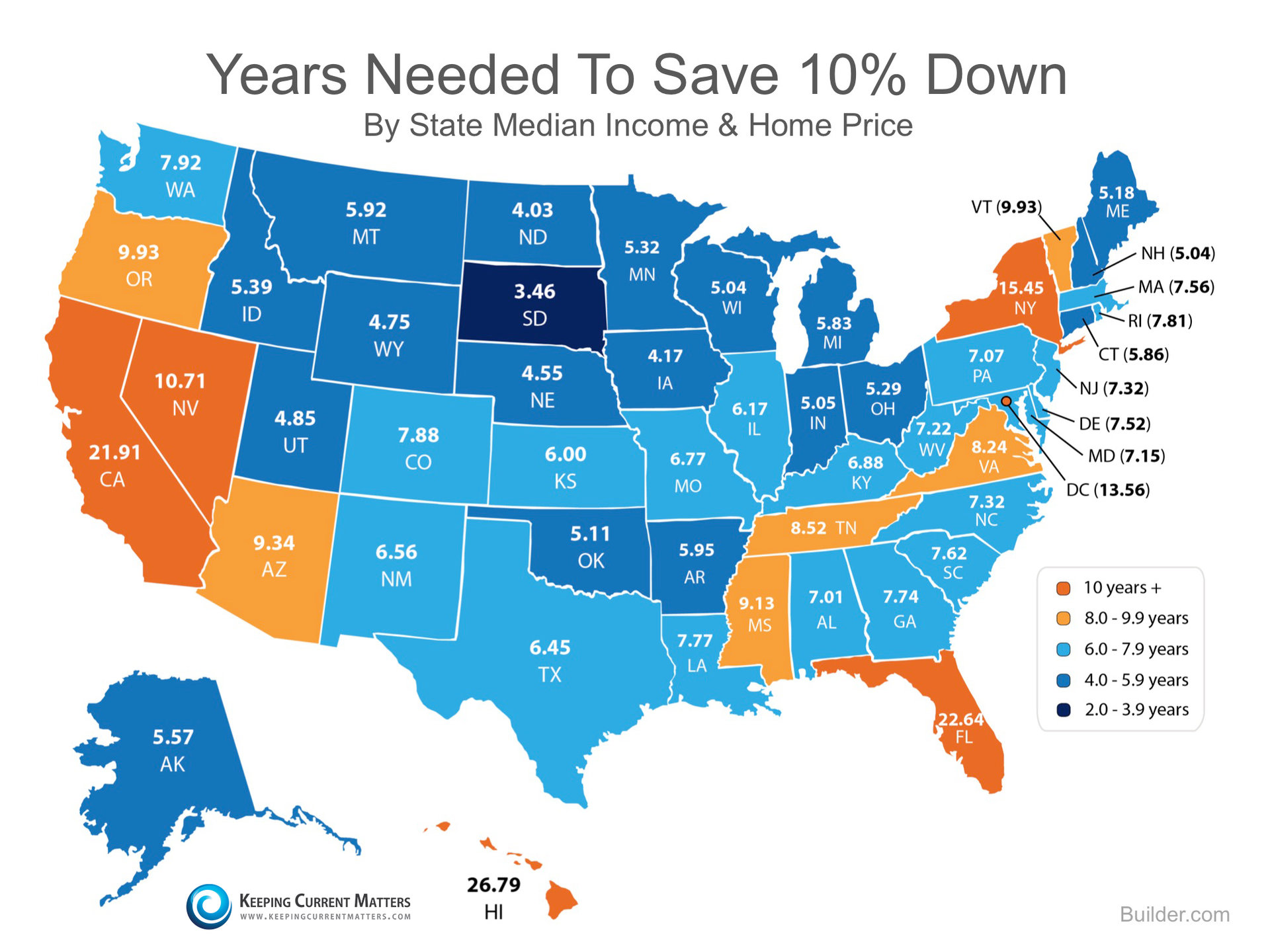

In a recent study conducted by Builder.com, researchers determined that nationwide it would take“nearly eight years” for a first-time buyer to save enough for a down payment on their dream home.

In a recent study conducted by Builder.com, researchers determined that nationwide it would take“nearly eight years” for a first-time buyer to save enough for a down payment on their dream home.

Depending on where you live, median rents, incomes and home prices all vary. By determining the percentage a renter spends on housing in each state and the amount needed for a 10% down payment, they were able to establish how long (in years) it would take for an average resident to save.

According to the study, residents in South Dakota are able to save for a down payment the quickest in just under 3.5 years. Below is a map created using the data for each state:

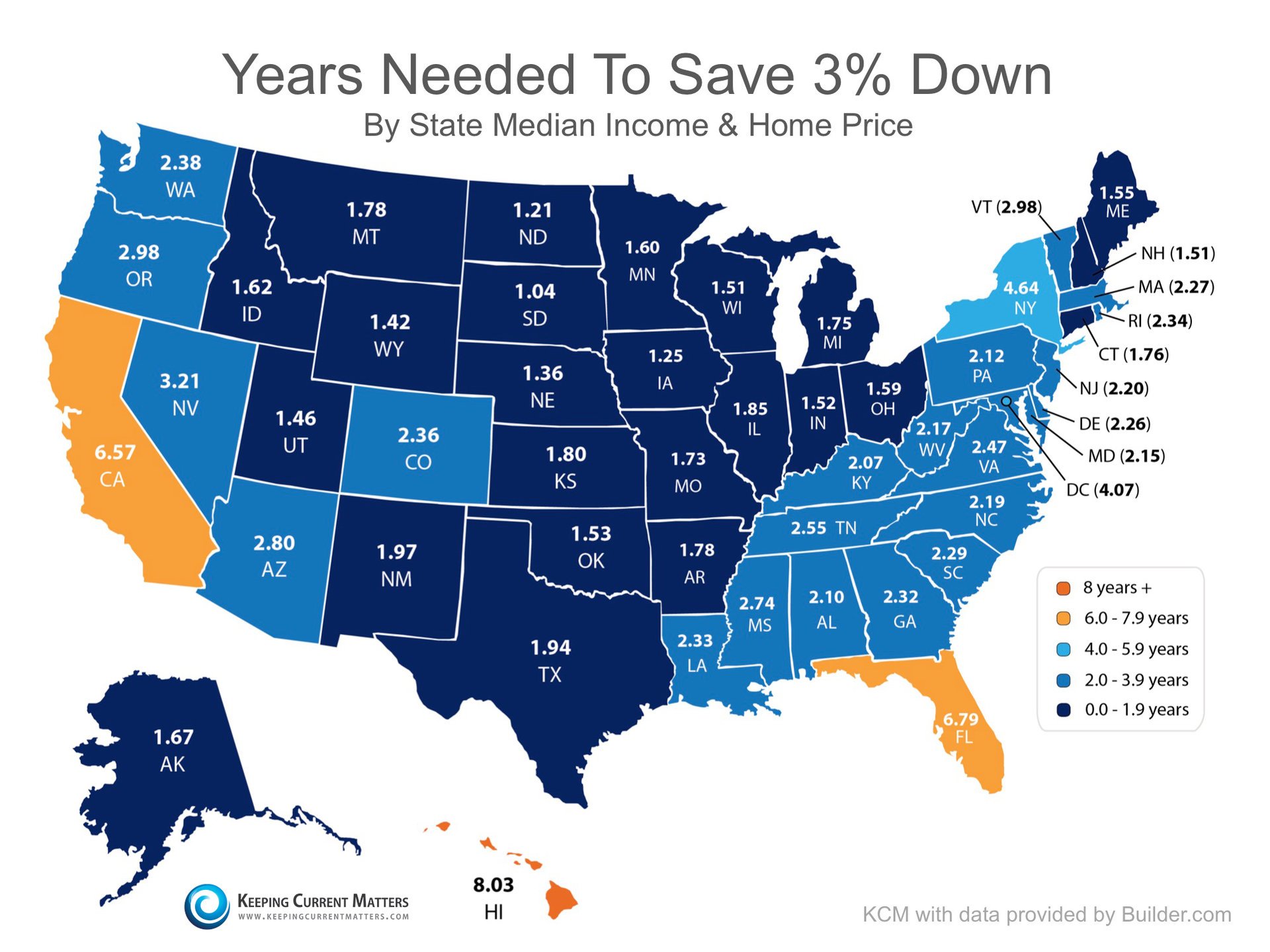

What if you were able to take advantage of one of the Freddie Mac or Fannie Mae 3% down programs? Suddenly saving for a down payment no longer takes 5 or 10 years, but becomes attainable in under two years in many states as shown in the map below.

Whether you have just started to save for a down payment, or have been for years, you may be closer to your dream home than you think! Meet with a local real estate professional who can help you evaluate your ability to buy today.

From traditional tile to trendy glass — and shiny metal to rustic wood — there is seemingly no end of choices for kitchen backsplashes today. “Tile is still the most popular backsplash material, with natural stone a fast-growing second,” says John Morgan, 2013 National President of the National Kitchen and Bath Association. “But with the right installer, you can make just about any material work.”

Kitchen backsplashes no longer simply protect walls from spills and splatters, a wide array of eye-catching materials like glass, wood, metals and stone make the backsplash the focal point of today’s kitchens.

In the monthly REALTORS® Confidence Index Survey, NAR asks REALTORS® “In the neighborhood or area where you make most of your sales, what are your expectations for residential property prices over the next year?” The map below shows the median expected price change in the next 12 months for each state, reported in the October 2015 REALTORS® Confidence Index Survey Report. REALTOR® respondents from Florida were the most upbeat, with a median expected price growth in the range of five to six percent. In Washington, Nevada, and Colorado, the median expected price growth among respondents was four to five percent.

Nationally, REALTORS® who responded to the October 2015 survey expected prices to increase by 3.2 percent over the next 12 months (3.2 percent in September 2015; 3.0 percent in October 2014). REALTORS® expect the recent strong price growth to moderate as rising prices have made homes “unaffordable” for many, with home prices almost at par with their levels prior to the housing downturn.

Colorful, luxurious and versatile, Boho chic style is perfect for spacious home interiors and small rooms. Boho chic ideas can help add luxury to small rooms, and create inviting and cozy home interiors in spacious living spaces. Here are some inspiring Boho chic ideas for modern interiors decorating and interior redesign in small spaces.

Colorful, luxurious and versatile, Boho chic style is perfect for spacious home interiors and small rooms. Boho chic ideas can help add luxury to small rooms, and create inviting and cozy home interiors in spacious living spaces. Here are some inspiring Boho chic ideas for modern interiors decorating and interior redesign in small spaces.

There has been much written about how dramatically home values have increased over the last several years. With the increase in values, comes an increase in the equity each home owning family now has. The Joint Center of Housing Studies at Harvard University recently reported that, after taking inflation into account, aggregate home equity has increased 60% since 2010. Home equity is the major component of most family’s overall wealth.

There has been much written about how dramatically home values have increased over the last several years. With the increase in values, comes an increase in the equity each home owning family now has. The Joint Center of Housing Studies at Harvard University recently reported that, after taking inflation into account, aggregate home equity has increased 60% since 2010. Home equity is the major component of most family’s overall wealth.

Throughout history, families have tapped into their homes for many important reasons. Perhaps it was to get seed capital to start a new business; perhaps to help finance their children’s college education; perhaps to get needed medical attention not covered by insurance.

Up to ten years ago, families were able to use the equity in their homes to better the living situation for themselves and their family. More small businesses were created. College students weren’t forced to take on massive student debt. People could get needed medical care.

This hasn’t been the case over the last ten years as families found themselves in a position of having zero equity or, even worse, negative equity post the housing collapse. However, that is about to change.

We realize that there are inherent risks to tapping into the equity in your home especially if you do it for the wrong reasons. Back in 2005-2007, homeowners were using their homes as their own personal ATM machine to buy depreciating assets like cars, boats and jet skis. This reckless behavior should never be repeated.

However, using your equity (aka family wealth) to invest in yourself, your children or other family members that could use help still makes sense. And the good news is that more and more families can do this as home values continue to increase.

Home equity gives families an additional financial option when money is needed. The proper use of this family wealth can be used to grow generational wealth.

As Julián Castro, U.S. Secretary of HUD, recently explained:

“Generation after generation, the primary vehicle to create wealth in our country has been through homeownership. In the U.S., homeownership has provided an opportunity for one generation to hand over to the next that opportunity and that wealth.”

The most recent Housing Pulse Survey released by the National Association of Realtors revealed that the two major reasons Americans prefer owning their own home instead of renting are:

The most recent Housing Pulse Survey released by the National Association of Realtors revealed that the two major reasons Americans prefer owning their own home instead of renting are:

In a recent article, John Taylor, CEO of the National Community Reinvestment Coalition, explained that those who lack the opportunity to become homeowners have a weakened ability to reinvest their wealth:

“We traditionally have been huge supporters of homeownership. We see it as a way to provide stability for households but also as an asset-building strategy. If you continue to be a renter, locked out of the homeownership arena, increasingly those things are further and further out of reach. They’re joined at the hip. They perpetuate each other.”

Does owning your home really create a more stable environment for your family?

A survey of property managers conducted by rent.com last month disclosed two reasons tenants should feel less stable with their housing situation:

We can see from these survey results that renting will provide anything but a stable environment in the near future.

Homeowners enjoy a more stable environment and at the same time are given the opportunity to build their family’s net worth.