The Baby Boomer generation, first of all, is defined in two categories in the 2015 Home Buyer and Seller Generational Trends Report; people born from 1955-1964 are called Younger Boomers and those born from 1946-1954 are Older Boomers. We will refer to the general group as “Baby Boomers” unless distinct research indicates differences for the two subcategories.

Combined, Baby Boomers account for 31 percent of the home buying population. This category gets overshadowed as a home buying demographic because they do not stand out as first-time buyers, as the Millennials do – which are a hot topic in the media and largely are first-time home buyers, and they are often not seen as buying large family homes with children under the age of 18 like Generation X. As a demographic, statistically speaking, their relative importance compared to Millennials appears to be less substantial because they are broken down into two categories.

Notably, Younger Boomers purchased more multi-generational homes in 2014 than any other age group at 21 percent. Baby Boomers in general have a strong purchasing power. Older Boomers have the same median income as Millennials approximately $76,000 for each and Younger Boomers have a higher purchasing power with a median income of $96,600.

NAR’s Generational Trends Report also shows that Baby Boomers are buying detached single-family homes more than any other home type. Eighty-one percent of Younger Boomers bought single-family homes as did 72 percent for Older Boomers. Baby Boomers are selling their larger homes and downsizing for smaller places predominantly in the suburbs or small towns. Younger Boomers cited that the primary reason for purchasing a home was a job-related relocation (16 percent) followed by the desire for a smaller home (13 percent). For Older Boomers, they bought homes first for retirement (15 percent) and second to be closer to friends and family (nine percent).

Additionally, there are senior-related housing communities that cater specifically to the Baby Boomer and the Silent Generation. For all buyers over the age of 49 who purchased in senior related housing, their housing preferences are delineated in the chart below:

Compared to other home buyers, Baby Boomers combined are 31 percent of the home buying population just after Millennials at 32 percent. Younger Boomers has the largest population of single females purchasing homes at 23 percent followed by Older Boomers at 21 percent. Single female Millennials are just half that pool of Baby Boomers at 12 percent. Single female Baby Boomers also purchased homes priced $100,000-150,000 more than any other price range.

Types of Homes Purchased by Baby Boomers

Older Boomers’ top reason for buying a new home more than any other age group (29 percent) was to enjoy the amenities of new home construction communities, to avoid renovations or problems with plumbing or electricity (28 percent), followed by the desire to customize the design features (25 percent). Factors that influenced Older Boomers were largely quality of the neighborhood, convenience to friends and family, shopping, and health facilities. Younger Boomers also prioritized the quality of the neighborhood but wanted convenience to jobs, schools, and shopping. Predominantly, Baby Boomers purchased homes ranging from $200,000-300,000 with three rooms and two bathrooms. About one-quarter of Baby Boomers bought homes that were built between 1960 and 1986 that are 1,501-2,500 square feet.

Heating and cooling costs were more important to Baby Boomers than other generations. Gen Y and Millennials were most concerned with commuting costs. Baby Boomers were more likely than other generations to report that they made no compromises on the home they purchased, whereas Millennials noted they compromised on price and size. Younger Boomers foresee that moving could be caused by life changes such as relocation for work whereas Older Boomers viewed their purchased as permanent and their ‘forever home.’

The Home Search Process for Baby Boomers

For Baby Boomers, they were twice as likely to contact a real estate agent first when starting the home search process compared to Millennials. All buyers looked online at 43 percent and Older Boomers drove by homes in various neighborhoods. Baby Boomers in general were half as likely as Millennials to use a mobile device to search for information about homes and utilized online video sites and newspaper ads more than other generations. Almost all generations equally visited 10 homes before they purchased.

Millennials found their homes on the internet 51 percent of the time compared to Older Boomers that found their homes first with a real estate agent 39 percent of the time and only 34 percent on the internet. Thirty-two percent of Older Boomers looked at foreclosures whereas 59 percent of Millennials considered it. All generations noted that the most difficult part of the home buying process was finding the right property. Millennials noted that understanding the process was difficult 27 percent of the time whereas Baby Boomers only cited this as an impediment seven percent of the time. Most notably, Baby Boomers used virtual tours 25 percent more frequently than Millennials. The Silent Generation reported they were the most satisfied with the home buying process above all other generations at 68 percent compared to 52 percent of Millennials.

Men have their man caves, but how about a space just for females? Welcome, the “she shed.”These backyard retreats are becoming the latest buzzword in interior design — emerging as the perfectly carved out haven for the woman of the household who seeks a quiet place of her own. Women are transforming old backyard sheds or even building mini cottages to create a place of relaxation or where they can pursue hobbies, such as ceramics, painting, and gardening. They are designing these mini sheds with everything from crystal chandeliers to luxurious furniture to create a top-notched designed space with all those feminine touches their heart desires. The only rule: No men allowed.

Men have their man caves, but how about a space just for females? Welcome, the “she shed.”These backyard retreats are becoming the latest buzzword in interior design — emerging as the perfectly carved out haven for the woman of the household who seeks a quiet place of her own. Women are transforming old backyard sheds or even building mini cottages to create a place of relaxation or where they can pursue hobbies, such as ceramics, painting, and gardening. They are designing these mini sheds with everything from crystal chandeliers to luxurious furniture to create a top-notched designed space with all those feminine touches their heart desires. The only rule: No men allowed. Fall is a good time to take care of big home repair projects before shorter days (and in many areas, ice and snow) make outdoor work too difficult. And if you do live in an area with cold winters, take some time this fall to boost energy efficiency throughout your home, and prevent damage from winter storms with proper tree care (we spoke with an expert to find out what you need to do). Tick these

Fall is a good time to take care of big home repair projects before shorter days (and in many areas, ice and snow) make outdoor work too difficult. And if you do live in an area with cold winters, take some time this fall to boost energy efficiency throughout your home, and prevent damage from winter storms with proper tree care (we spoke with an expert to find out what you need to do). Tick these ![Economic Impact of Every Home Sold [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/09/Economic-Impact.jpg)

If you are debating purchasing a home right now, you are surely getting a lot of advice. Though your friends and family will have your best interest at heart, they may not be fully aware of your needs and what is currently happening in real estate.

If you are debating purchasing a home right now, you are surely getting a lot of advice. Though your friends and family will have your best interest at heart, they may not be fully aware of your needs and what is currently happening in real estate.

![A+ Reasons To Hire A Real Estate Professional [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/08/A-Reasons-To-Use-A-RE-Pro.jpg)

Home Exterior Makeovers Browse before-and-after photos of these home makeovers and

Home Exterior Makeovers Browse before-and-after photos of these home makeovers and

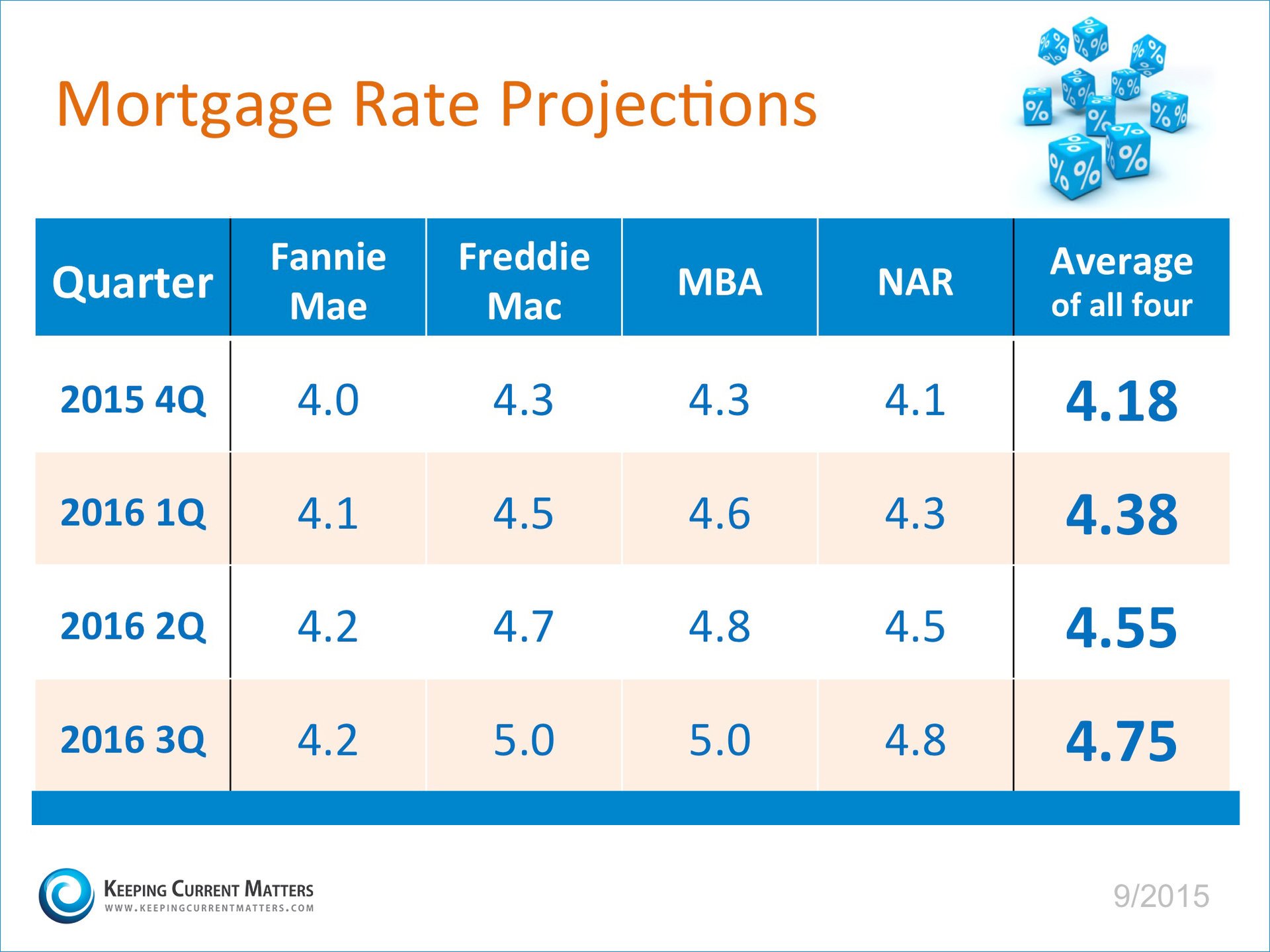

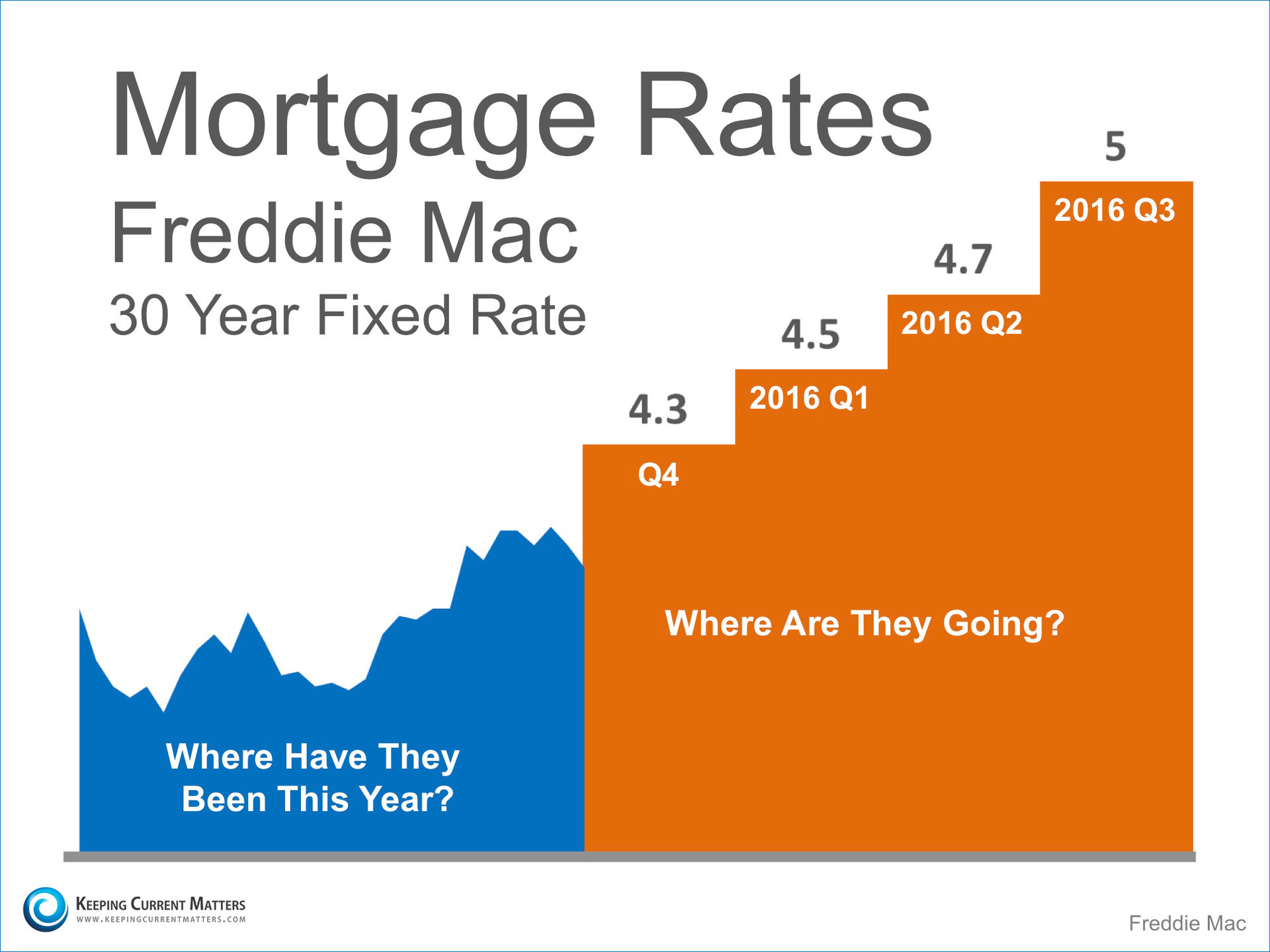

The interest rate you pay on your home mortgage has a direct impact on your monthly payment. The higher the rate the greater the payment will be. That is why it is important to look at where rates are headed when deciding to buy now or wait until next year.

The interest rate you pay on your home mortgage has a direct impact on your monthly payment. The higher the rate the greater the payment will be. That is why it is important to look at where rates are headed when deciding to buy now or wait until next year.

People always talk about the “spring buying season” when they talk real estate. However, this year it appears as though the

People always talk about the “spring buying season” when they talk real estate. However, this year it appears as though the  First-time homebuyers are flocking to the housing market in greater numbers than any time in the last few years. Renters who are ready and willing to buy are now realizing that they are also able to as well. Many first-time buyers are Millennials (born between 1981 – 1997).

First-time homebuyers are flocking to the housing market in greater numbers than any time in the last few years. Renters who are ready and willing to buy are now realizing that they are also able to as well. Many first-time buyers are Millennials (born between 1981 – 1997).